The Net Present Value (NPV) is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. The NPV is used in capital budgeting and investment planning to analyze the profitability

of a projected investment or project.

NPV is the result of calculations used to find today’s value of

a future stream of payments. It accounts for the time value of money and can be used to compare similar investment alternatives. The NPV relies on a discount rate that may be derived from the cost of the capital required to make the investment, and any project or investment with a negative NPV should be avoided.

HOW TO CALCULATE THE NET PRESENT VALUE

WHAT IS THE NET PRESENT VALUE?

The mathematical formula for NPV therefore involves finding the discount rate, or interest rate, that sets all the project’s cash flows to an NPV of zero.

NET PRESENT VALUE FORMULA:

n

Rt

NPV = _________

t

(1 + i)

t=1

NPV = Net Present Value

Rt= Net cash inflows-outflows during a single period t

i = Discount rate or return that could be earned in alternative investments

t = Number of timer periods

An investment with a negative NPV will result in a net loss. This concept is the basis for the Net Present Value Rule, which dictates that only investments with positive NPV values should be considered. Calculation of the NPV is a two step process.

The following is an example.

EXAMPLE

Imagine a real estate company acquires a commercial property that will cost $1,000,000 and is expected to generate $25,000 a month in revenue for five years. The company has the funds available for the property and could alternatively invest it in the stock market for an expected return of 8% per year. However, the managers feel believe that the stock market is a more riskier alternative.

Step One: NPV of the Initial Investment

Because the property is paid for up front, this is the first cash flow included in the calculation. No elapsed time needs to be accounted for so today’s outflow of $1,000,000 doesn’t need to be discounted.

Identify the number of periods (t): The property is expected to generate a monthly cash flow and last for five years, which means there will be 60 cash flows and 60 periods included in the calculation.

Identify the discount rate (i): The alternative investment is expected to pay 8% per year. However, because the property generates a monthly stream of cash flows, the annual discount rate needs to be turned into a periodic or monthly rate. Using the following formula, we find that the periodic rate is 0.64%.

1/12

Periodic Rate = ((1+0.08) ) - 1 = 0.64%

Step Two: NPV of Future Cash Flows

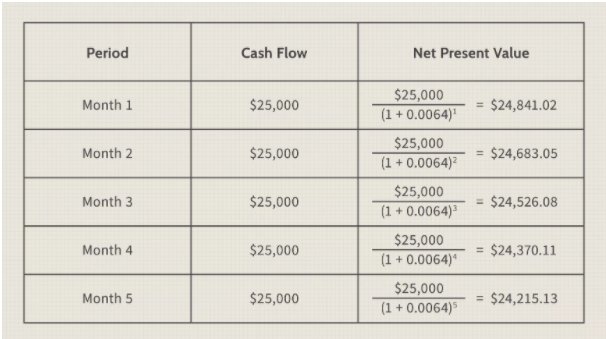

Assume the monthly cash flows are earned at the end of the month, with the first payment arriving exactly one month after the equipment has been purchased. This is a future payment, so it needs to be adjusted for the time value of money. An investor can perform this calculation easily with a spreadsheet or calculator. To illustrate the concept, the first five payments are displayed in the table as shown (right).

The full calculation of the present value is equal to the present value of all 60 future cash flows, minus the $1,000,000 investment.

60 25,000 60

NPV = −$1,000,000 + ___________

t=1 60

(1 + 0.0064)

This formula can be simplified to the following calculation:

NPV=−$1,000,000+$1,242,322.82 = $242,322.82

HOW USEFUL IS THE NET PRESENT VALUE?

The NPV is a financial metric that seeks to capture the total value of a potential investment opportunity. The idea behind NPV is to project all of the future cash inflows and outflows associated with an investment, discount all those future cash flows to the present day, and then add them together. The resulting number after adding all the positive and negative cash flows together is the investment’s NPV. A positive NPV means that, after accounting for the time value of money, you will make money if you proceed with the investment.