Under Section 1031 of the United States Internal Revenue Code (IRS), a taxpayer may defer their capital gains tax and related federal income tax liability on the exchange of certain types of property.

WHAT IS A 1031 TAX-DEFERRED EXCHANGE?

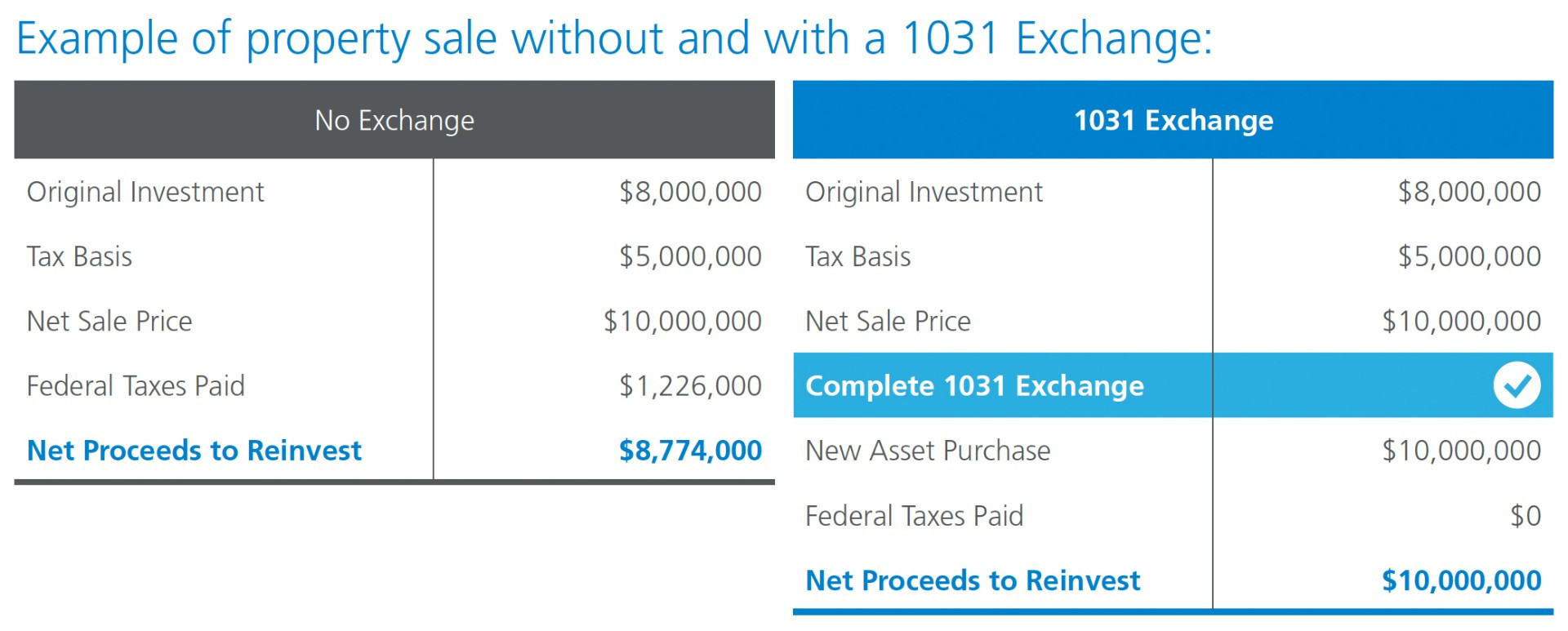

The 1031 Tax-Deferred Exchange is a method by which one can dispose of their investment assets when selling a property by acquiring a like-kind replacement property within 180 days. Further, through the use of a qualified intermediary during the exchange process, this method would defer the tax that would ordinarily be due upon such a sale.

Although the current interest in the 1031 tax exchange could give the impression that Section 1031 is a recent development, the 1031’s history stretches all the way back to 1921. The 1031 Exchange received attention in the late 1970 and mid 80's when significant modifications in the manner in which the exchanges were conducted required Congress to amended the exchange timeline to 180 days. The modifications resulted in a powerful improvement of the exchange process and also generated increased interest from real estate investors.

HOW DOES A 1031 EXCHANGE WORK?

IRS Section 1031 provides for the postponement

of paying gains tax if sale proceeds are invested in similar property as part of a qualifying like-kind exchange. Tax sheltered income and long-term growth can be the benefits. A 1031 exchange gets its name from Section 1031 of the U.S. Internal Revenue Code, which allows you to avoid paying capital gains taxes when you sell an investment property and reinvest the proceeds from the sale within certain time limits in a like-kind property and equal or greater value.

The 1031 exchange timeline is broken into two parts: the identification period and the exchange period for the Exchanger to have a valid exchange in accordance with IRS requirements:

Identification Period

Within 45 calendar days of the disposition of the Exchanger's first relinquished property and its proceeds to a qualified intermediary in the interim, the Exchanger must identify like kind replacement property to be acquired.

Exchange Period

The Exchanger must then receive the replacement property within the earlier of 180 calendar days after the date on which the Exchanger transferred the first relinquished property, or the due date (including extensions) for the Exchanger’s tax return for the tax year in which the transfer of the first relinquished property occurs.

What is a Like-Kind Property?

According to the IRS, properties are of like-kind if they’re of the same nature or character, even if they differ in their grade or quality. For example, the relinquishment a commercial office building in exchange for mineral rights on another property.

What is a Qualified Intermediary?

A qualified intermediary facilitates the exchange to hold those proceeds of the initial sale until the exchange is complete. It acts as a way to avoid premature receipt of cash or other proceeds.